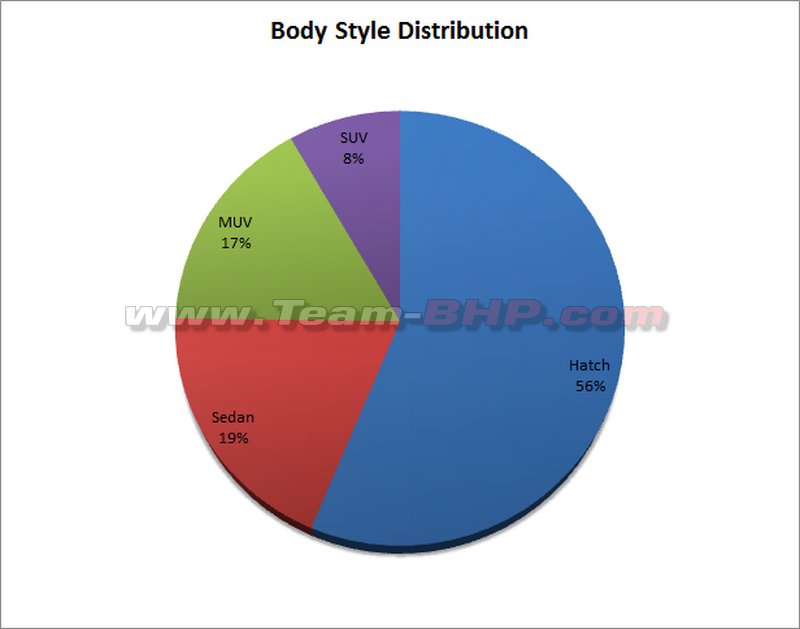

Movers & Shakers

A good start to 2013, as is usually the case with the first month of the year. After all, it’s easier to sell a Jan 2013 build car even in May 2013, than it is to move a Dec 2012 car in Feb 2013. Customers demand a build date of the current year, and rightly so!

With a cumulative figure of 2.3 lakh cars, Jan 2013 was the 2nd best month of this financial year (

after October 2012). Importantly, the bump in sales is 20% over the previous month. Overall year-on-year sales are off by 5%; that’s actually good news when you consider the current state of the market and compare it to the buoyant times of early 2012.

The RBI announced a marginal cut in the repo rate (0.25) and cash reserve ratio (to 4%). On the flip side, the deregulation of diesel pricing means the fuel will see slow & steady price increases over the coming year.

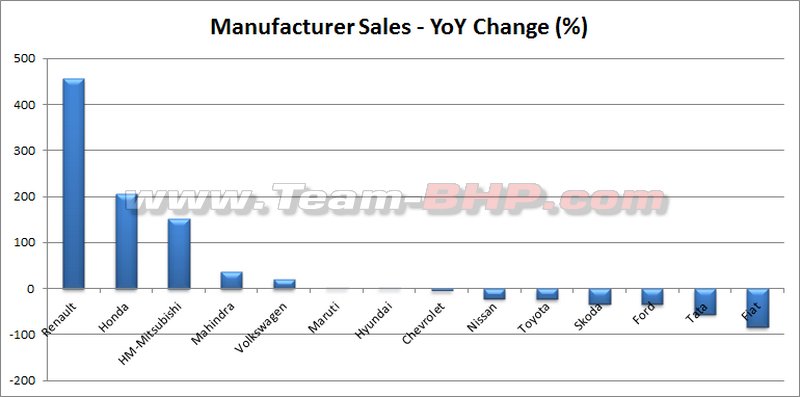

Maruti’s domestic numbers actually grew 2% over the corresponding period of 2012, while the month-on-month tally rises by 25%. January was also the first month of the current financial year where Maruti enjoyed 6-digit volumes. However, exports dived noticeably by about 22%. Maruti’s domination, even after all of the world’s brands have arrived in India, is commendable. The Alto, WagonR, Swift & Dzire scale new heights, with three of them recording their highest sales performance in 6 months. The company's latest UV – the Ertiga – also has a good run, even if it’s slipped off the previously held 7k level. The facelift, variant shuffling & AT gearbox don’t seem to be doing much for the Ritz. Fact is, the car is getting old in design terms, and a full generation behind the Swift. The SX4 experiences growth, but 1,000 units isn’t saying too much for a Maruti sedan. Probably dealers stocking up the marginally updated version? The lack of a diesel option has stalled the resurgence of the Eeco (aka Versa).

Hyundai also records a marginal Y-O-Y growth and quite an impressive M-O-M jump. Petrol cars continue to crawl back slowly & steadily. The entry-level Eon moves past the 8,000 mark, but the i20 – Hyundai’s most expensive hatchback – outsells all of its (cheaper) siblings! The Fluidic Verna & Elantra remain the sedans to beat in the C2 & D1 segment (respectively). These two have given the market exactly what it wanted. On the flip side, the Sonata brings back D2 segment nightmares for Hyundai. Some things, I guess, will never change.

Mahindra’s got its foot on the accelerator and there’s no letting back. Get this: For the entire of year 2011, Mahindra sold about ½ as much as no.2 car maker Hyundai. The home boys appear to be firmly ensconced at the 25,000 average now. That’s only 8,000 units shy of the Koreans. Primary reason? One blockbuster UV launch after another. The Bolero goes from strength to strength, yes. But the shortened Xylo (i.e. Quanto) adds another 3,000 to the kitty. The Scorpio & XUV500 are habitual 4,000 / month scorers. Their latest SUV, the premium’ish Rexton, has a good month at 457 sales and has outsold every SUV in its class, save for the mighty Fortuner. For a niche product, the Thar is a decent runner @ 600+ copies.

Breaking the trend set by the top 3 is Tata Motors. Y-O-Y sales are less than 50% of the Jan 2012 levels, while the M-O-M climb is slimmer than the others too. A dismal 15,000 shipments makes Jan the second-worst month in a year for Tata (

after the equally poor December 2012). This is the net result of poor reliability & quality levels and an ageing product line (for the most part). The Indica + Vista and Safari + Storme are the only products to have earned their lunch. Everything else – from the Nano to the Aria – has under-performed. It’s shocking to see the Indigo + Manza at a low 2,367 units. If it weren’t for its commercial vehicle division & Jaguar-Land Rover, Tata would have been in the red. The passenger car division remains Tata’s weakest (albeit most visible).

Toyota reports a small increase from December, but 13K is well off the 17K of last January. There’s a clear reason for that: While the Innova & Fortuner (1,500 pieces!!!) keep the cash registers ringing, the big T is going to have to bring contemporary hatchbacks & sedans (like the Swift, i20 etc.) to the Indian market. The old-school Liva & Etios can’t cut the mustard. The unbreakable Corolla Altis has its share of fans in the market; 384 is a fair number by current D1 standards.

Chevrolet has new additions to its portfolio, and three MUCH REQUIRED deletions (Optra, Aveo, Aveo UVA). Status quo for the Beat diesel which is Chevrolet’s star performer, followed by the dependable Tavera. Not much to write home about otherwise, not even from the Cruze which was a champion at one time. Obviously a facelift strategy gone wrong. The Sail UVA fails to make any sort of mark in the fiercely competitive B2 hatchback segment. Competent yes, though buyers are clearly not giving the dated design & interiors a second look. We’ll be keenly watching the market performance of the well-priced Sail sedan.

The Polo revvs up and how! 4,600 units is a great month for VW’s hatchback. I consider the Vento as an under-performer in the market though, as it is still the best diesel C2 sedan, although the lukewarm numbers simply don’t show it. 233 isn’t bad for the Jetta, considering its pricey tag…it has outsold sister Laura for the 2nd month in a row. Overall, VW records notable Y-O-Y and M-O-M gains, primarily due to the Polo. There’s still a lot of work left to do.

The Figo is Ford’s “everything” at the moment. The Endeavour & Fiesta Classic suffer a sharp nosedive from their usual levels. New Fiesta hits new lows. A poor start to 2013 for the American company, whichever way you look at it.

2,900 cars makes a respectable month for the City, considering its petrol-only offering. The Brio is the other car keeping the Honda dispatchers busy, yet 2,300 is a poor show for a Rs. 5 lakh hatchback. All other Hondas are in the two-digit range, including the Jazz! At 61 pieces, the Jazz is the worst selling hatchback in India, outsold by other flops like the Fabia & Punto. The otherwise brilliant machine simply never recovered from its initial pricing debacle. The 30 units you see of the CRV are of the next-generation car. It’s also locally assembled (not CBU), so perhaps, the pricing might be more realistic. You can expect an official review later in February.

There’s no real setback in demand for the Duster, thus we can nail down the fall to 3,500 units as supply limitations. The Scala appears to be settling at the 800 level. Sister concern Nissan sees the Sunny stepping up to 2,500 shipments, while the Micra also has a spike in its (normally dismal) performance. The Evalia – touted as an Innova competitor – seems to be a complete write-off. Period.

Can’t figure out what Skoda is up to. We keep hearing of big changes & management reshuffling, but the market numbers don’t show any signs of improvement. The Rapid’s love with the 1.5K point is inexplicable for such a well-priced competent car. The luxo-barge Superb, though still in the lead, isn’t dominating the D2 segment as it did earlier. The Passat & Accord aren’t that far behind anymore. Only 2,000 cars keeps Skoda ahead of just the permanent back-benchers, HM & Fiat.

For having the support of a nearly defunct manufacturer, the Pajero Sport is a splendid performer @ 230 copies. That is ~50 crore rupees in gross for HM. And the vintage Ambassador does outsell some other modern sedans (including the Linea). Fiat is down 85% from last Jan, which wasn’t a strong position to start with. In my opinion, Fiat should reposition itself as a niche manufacturer targeting segments where competition doesn't exist (e.g. how Renault got the Duster). As Bud Fox once said "If your enemy is superior, evade him".

Folks, we have one interesting year ahead of us!

2nd February 2013, 15:31

2nd February 2013, 15:31

(28)

Thanks

(28)

Thanks

Now this is unbelievable!! The Petrol outselling the Diesel Fluence comprehensively!! Is there a mistake from Renault in giving these numbers? Or did they do that on purpose to get our attention on the Fluence!!

Now this is unbelievable!! The Petrol outselling the Diesel Fluence comprehensively!! Is there a mistake from Renault in giving these numbers? Or did they do that on purpose to get our attention on the Fluence!!