This is the tale of a claim with Oriental Insurance regarding our 13 year old Honda City that was damaged by a tree falling on it during the rains in Bangalore last month.

TL;DR:

13 year old car damaged by a tree falling on it. Repair costs are Rs.1.34L. IDV of the car is 1.62L. Insurance Payable is Rs.91,000.

Terms and Conditions of the policy:

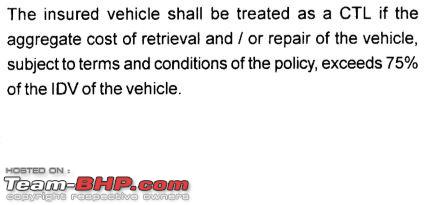

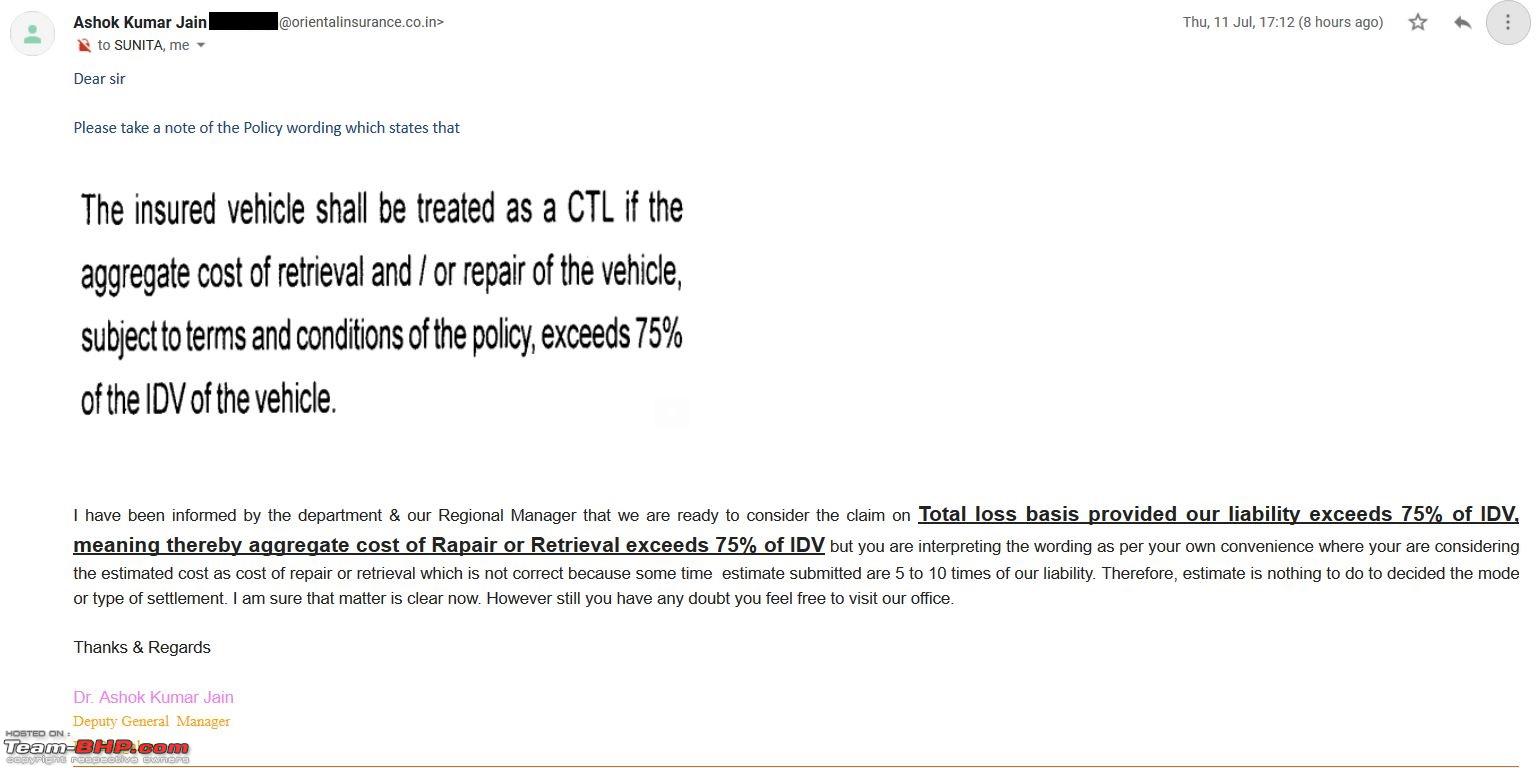

"The insured vehicle shall be treated as a Constructive Total Loss if the aggregate cost of retrieval and / or repair of the vehicle, subject to terms and conditions of the policy, exceeds 75% of the IDV of the vehicle."

But, Oriental Insurance is saying that since

their liability or insurance payable does not exceed 75% of the IDV of the vehicle, the claim will be a repair settlement.

Now, the longer version:

In the first week of June, I had used to car to get to work when it really started pouring down in the evening accompanied with heavy gusts of wind. I had already begun to think that the car will be damaged by trees since my office is in one of the few areas where green cover has been maintained in Bangalore. When I walked over to the car in the evening post work, this is what I saw:

Luckily, the car was in drivable condition and I drove it back home. Then started the process of finding someone who would repair it. Of the two private garages, both said it is best to leave it at Honda’s authorized service centre. So I took their advice and contacted Dakshin Honda – the same place we purchased our Honda Jazz from. I sent them pictures on WhatsApp and they came back with a quote of Rs.1,50,000 or so – which was in turn with what one of the private garages had told me I should expect. I then checked with Magnum Honda since they had good reviews on their Body Shop listing on Google. I sent them the same pictures and they came back with a quotation of Rs.58,000 based on the pictures I had sent on WhatsApp. I told them I would drop by on the 12th of June to drop off the car for repairs.

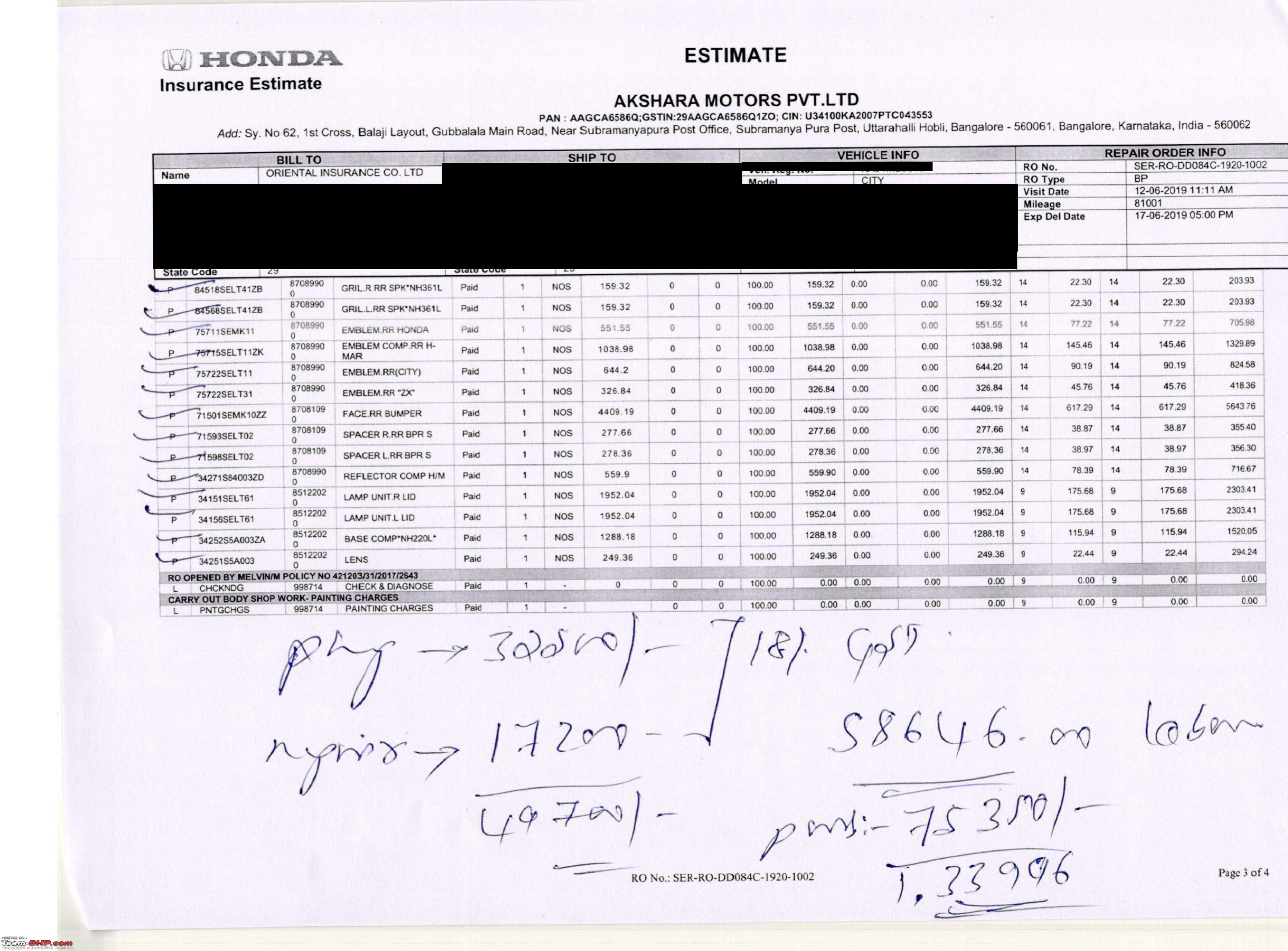

I dropped off the car for repair on the 12th and the service advisor told me I should expect a bill of close to Rs.1,50,000 for all the repairs. We also started the insurance claim process by this time. The IDV of the car was Rs.1,62,000. The insurance company said they need a detailed estimate before they assess the car. I asked Magnum Honda for this and they sent me a detailed estimate carrying repair costs of Rs.1,59,000.

We forwarded this to Oriental Insurance and asked them to proceed with the surveyor.

At this point, I had gathered that since the repair cost was greater than 75% of the IDV = Rs.1,21,500, the claim would be settled as a total loss.

The surveyor visited the service center and told us the repair estimate was Rs.1,34,000 and the insurance payable was around Rs.80,000 to Rs.90,000. Since the insurance payable was not greater than 75% of the IDV, the car would be repaired.

I had read about the terms and conditions for total loss and knew it was based on total cost of repair of the car and not insurance payable.

From IRDA’s Policy Wording for Private Car polices:

From Oriental’s Terms and Conditions for Private Car insurance policies:

I tried explaining it to the surveyor, but he refused to accept what I was saying.

A few days later, we got this letter from Oriental:

I called Oriental Insurance’s customer care – who tried to tell me that the IDV would undergo depreciation since it is an old vehicle. I told them they are lying because it is clearly mentioned in the terms and conditions that no further depreciation will be made on the IDV. He then asked me to email Oriental on

csd@orientalinsurance.co.in. I promptly did this and awaited a reply for a few days. We also met a Mr. Raghavendra at the Claims office to understand what was happening. He told us that if we were going to look at clauses in the terms and conditions, we should go the legal route. When a reply did not come to my email to

csd@orientalinsurance.co.in, I called IRDA’s Policy Holder helpline which told me to contact the Regional Manager – Mrs. Sunita Gupta in their office on Residency Road. I had also raised a grievance on PG Portal by this time.

I e-mailed her the day prior to my visit with details of the case so she can familiarize herself with the details. I visited her the next morning along with my brother. She said that they had ignored my e-mails and grievances thus far because the Policy Holder’s name and mine did not match. Fair argument, I let it go.

Mr. Raghavendra, whom we had met earlier, also joined us in this conversation. When we asked her why this was not a total loss claim, she told us that they were just following what was told to them by the corporate office. But she would look into our case and get back to us by the end of the day – this was a Wednesday. I waited until Friday to email her and check with her – still did not receive a reply.

The car had already been at the service center for a month and was racking up parking charges every single day.

This Monday, we got information that the claim was going to be settled on repair basis and not on total loss basis. The next day, we raised an issue on IRDA’s grievance system – igms.irda.gov.in. In which we had mentioned that we want all communication to be via email and nothing to be sent physically. We also found the e-mail IDs of a bunch of senior executives of Oriental Insurance here:

https://orientalinsurance.org.in/web...ior-executives and emailed all of them hoping something good would come of it.

Upto Wednesday – no response. Except one person from the senior executives list saying the DGM of the Residency Road branch had retired and one, Mr. Ashok Jain was now the DGM. He was kind enough to give me his email ID as well. We forwarded the same email to Mr. Ashok Jain as well.

This afternoon, we got responses to our IGMS complaint through Mr. Sivakumar and also a reply from Mr. Ashok Jain, the DGM of the Residency Road branch:

We’ve sent them court rulings from previous cases (

https://indiankanoon.org/doc/180217210/) where it clearly says that the repair cost is to be considered for total loss settlements. But everyone at Oriental seems hell bent on continuing with their lies. IRDA also seems toothless in that aspect. What options do we have apart from the long and arduous legal process?

Goes without saying, if you are from Bangalore - please do not purchase your insurance from Oriental Insurance. They have zero regard for the terms and conditions and use that as a scare tactic to try and get people to shut up.

I've also attached the copies of IRDA's Policy Wording and Oriental's Terms and Conditions should anyone ever need them in future.

12th July 2019, 02:32

12th July 2019, 02:32

(11)

Thanks

(11)

Thanks